A certificate of insurance (COI) is a one-page summary document proving that a contractor, vendor, or subcontractor has active insurance coverage. It is not an insurance policy — it is evidence that a policy exists. In construction, COIs are required from every subcontractor before work begins and must be current, compliant with contract requirements, and reviewed for the right endorsements — not just collected and filed.

What is a certificate of insurance?

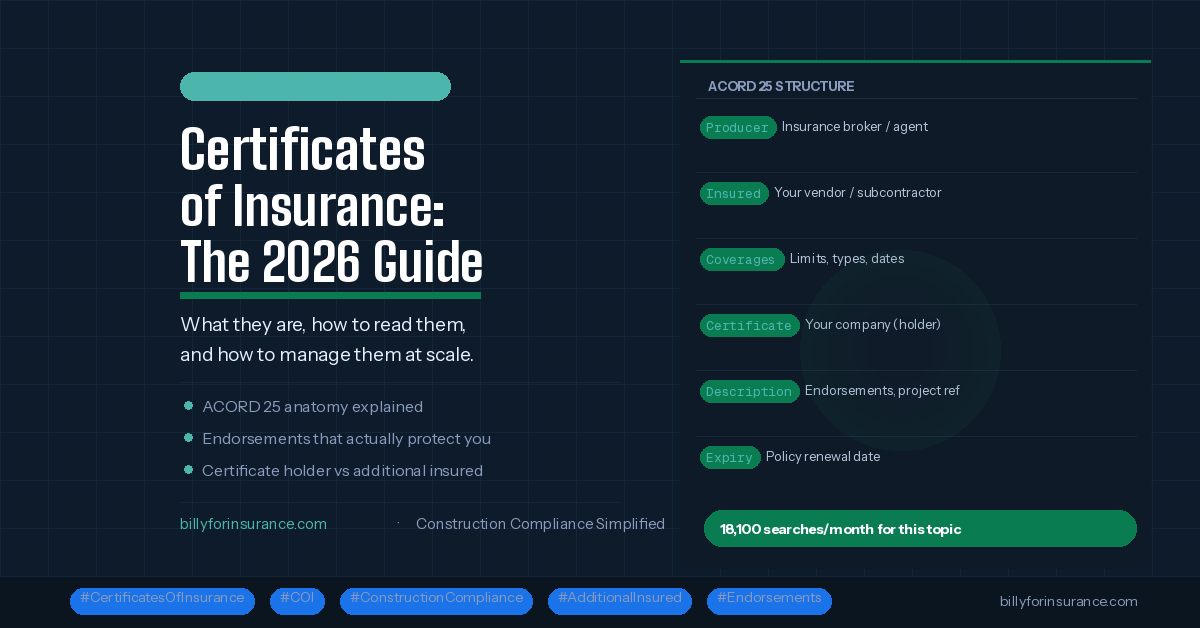

A certificate of insurance is a standardized document issued by an insurance broker on behalf of their client. It summarizes the types of coverage the client carries, the coverage limits, the policy effective and expiration dates, and who holds the policy.

In the United States, the standard form is the ACORD 25 — maintained by ACORD (Association for Cooperative Operations Research and Development) and used by virtually every U.S. insurance broker. When someone asks for a COI, they’re almost always asking for an ACORD 25.

It’s worth being precise about what a COI is not:

- It is not an insurance policy. The COI summarizes coverage; it does not establish it.

- It is not a guarantee of coverage. Only the actual policy determines what is and isn’t covered.

- It is not a substitute for endorsements. A COI that says “additional insured” in the description box doesn’t provide additional insured coverage — only an attached endorsement does.

These distinctions matter because many construction teams treat COI collection as a compliance checkbox. Collecting a COI and having a compliant vendor are not the same thing.

How to read a certificate of insurance

The ACORD 25 is divided into several sections. Here’s what each one means and what to look for:

Types of coverage on a COI

Construction COIs typically include several coverage types. Knowing what each one covers helps you verify that the right protection is in place for your specific project.

Certificate holder vs additional insured: the most important distinction in COI compliance

This is the distinction that causes the most claims exposure in construction. Many GCs believe that collecting a COI with their name on it as certificate holder protects them. It doesn’t.

A certificate holder receives a copy of the certificate and is notified if the policy is cancelled. That’s it. No coverage, no protection, no ability to file a claim under the vendor’s policy.

An additional insured is a party that has been added to the vendor’s insurance policy and can file claims under it. This means that if the vendor causes an injury or property damage while working on your project, you can seek coverage under their policy rather than your own.

A COI can say “additional insured” in the description box, but if the actual endorsement isn’t attached to the policy, that designation has no legal weight. The only thing that creates additional insured protection is an endorsement on the underlying policy. This is why collecting a COI isn’t enough — the endorsements behind it must be verified. See our full breakdown: certificate holder vs additional insured.

Endorsements: what they are and which ones matter

An endorsement is a modification to an insurance policy. It adds, removes, or changes coverage beyond what the standard policy provides. For construction COI compliance, endorsements are often more important than the base policy — and they’re where most compliance gaps hide.

The endorsements you’ll encounter most often in construction contracts:

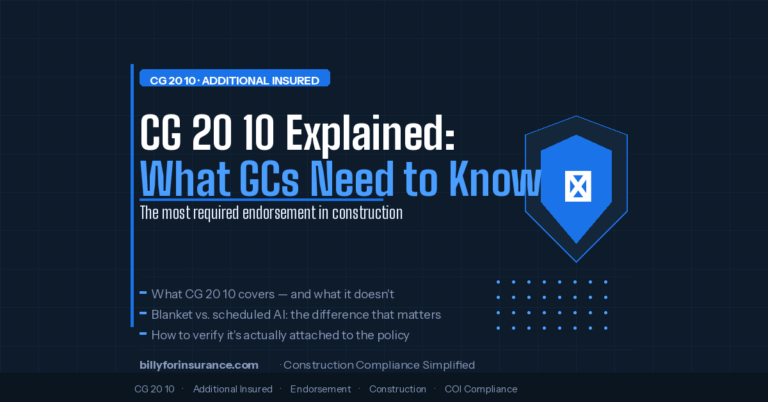

- CG 20 10 (Additional Insured — Ongoing Operations): Adds the GC as an additional insured under the subcontractor’s CGL policy for claims arising from ongoing work on the project. This is the most commonly required endorsement in construction subcontracts.

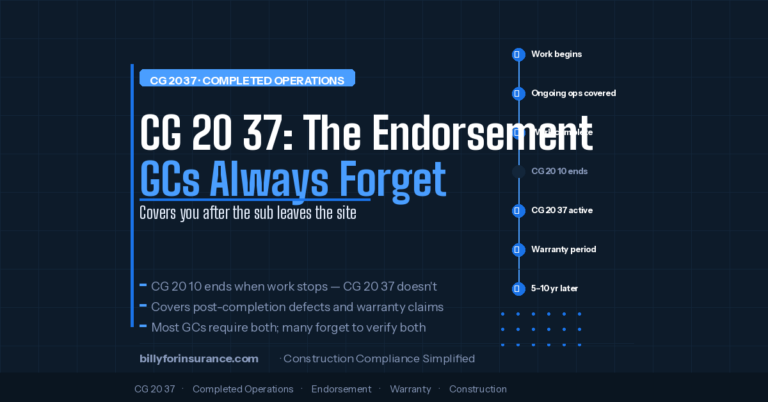

- CG 20 37 (Additional Insured — Completed Operations): Extends additional insured protection to cover claims arising after the project is complete — typically for 1–10 years after closeout. Required by most general contractors for any project with a defect liability period.

- Primary and Non-Contributory (P&NC): Makes the subcontractor’s policy the primary payer in a claim, rather than sharing costs with the GC’s policy. Without this, your own insurance gets pulled into claims caused by your subcontractors.

- Waiver of Subrogation: Prevents the vendor’s insurer from pursuing claims against your company after paying out a claim. Commonly required to avoid being sued by your own subcontractor’s insurer.

For a complete guide to these endorsements, see: CG 20 10, CG 20 37, and Primary & Non-Contributory explained.

What to check when you receive a COI

Most construction teams accept COIs without reviewing them. That’s the root cause of most COI-related claims exposure. Here’s what an actual review looks like:

The most common COI compliance gaps in construction

These are the gaps that come up repeatedly in claims investigations and compliance audits:

Expired certificates

The single most common gap. A certificate was collected when the vendor started, but nobody tracked the expiration date or requested a renewal. By the time it comes up, the vendor has been working uninsured for months.

Missing or wrong endorsements

A COI shows coverage, but the CG 20 10 endorsement isn’t attached. The description box says “additional insured” but there’s no actual endorsement on the policy. The protection that matters is in the endorsement, not the COI.

Insufficient coverage limits

A COI is on file, but the limits are below what the subcontract requires. This is almost never caught in manual review because reviewers compare the COI to what they received, not to what the contract requires.

Insured name mismatch

The contract is with ABC Concrete LLC. The COI is for ABC Concrete Inc. Those are technically different legal entities. In a claim, this distinction matters — and insurers will notice it.

No completed operations coverage

CG 20 10 covers ongoing operations but not completed operations. If a defect is discovered after project closeout and CG 20 37 wasn’t required or verified, the protection for that period may not exist.

COI collected, never reviewed

The most systemic gap. A COI arrives via email, gets filed in a shared folder, and is marked as collected. No one checked the limits, the endorsements, or the insured name. It’s in the system but not actually compliant.

Managing certificates of insurance at scale

When you’re managing COIs for dozens or hundreds of vendors, the manual process described above — request, receive, review, file, remind — breaks down at every stage. The volume of incoming certificates, combined with the ongoing renewal cycle, creates a compliance operation that one or two people cannot run effectively without automation.

The challenges that appear at scale:

- 15–25 certificate expirations per month per 200 active vendors

- Multiple concurrent projects with different contract requirements

- Vendors with multiple insurance agents for different coverage types

- AP holds that fire at payment time rather than being caught in advance

- Audit requests requiring historical compliance records, not just current status

Automating the COI lifecycle — collection, review, renewal outreach, ERP sync — reduces the operational burden to exception handling rather than full management. For a step-by-step guide to building that process, see: certificate of insurance tracking at scale.

For teams running Viewpoint Vista, Sage 300, Sage Intacct, Procore, Autodesk, or JD Edwards, Billy’s COI tracking software integrates directly with each platform — so compliance status lives in the system where payment decisions are made, not in a separate tool your AP team has to check separately.

If you’re managing fewer than 25 vendors and want to start with a structured manual process, our free COI tracking template for Excel covers the basics. For teams past that threshold, it has real limits — but it’s a useful baseline for structuring what you collect and when you follow up.

Frequently asked questions

Stop managing COIs manually

Billy automates the entire COI lifecycle — collection, review, renewals, and ERP sync — so your team focuses on exceptions, not paperwork.

Summary

Certificates of insurance are the foundation of vendor risk management in construction. A COI proves that a vendor has coverage — but collecting one is not the same as having a compliant vendor. The most important distinctions: certificate holders get notifications, additional insureds get coverage; endorsements create protection, COIs only summarize it; and a filed COI that hasn’t been reviewed for limits, endorsements, and insured name is a gap that often doesn’t surface until a claim or audit.

Managing COIs at scale requires automating the collection, review, and renewal cycle rather than running it manually. For teams past 25–50 active vendors, the operational cost and risk exposure of manual tracking consistently outweigh the investment in a structured compliance system.