Subcontractor Insurance Requirements by Trade: The 2026 Checklist for General Contractors

14 min read · Construction Compliance · Updated Feb 2026

Most GCs use a single insurance requirement template for every subcontractor on every project. The same $1M/$2M CGL limits. The same $1M auto. The same $5M umbrella. It doesn’t matter if the sub is a demolition contractor bringing wrecking balls to a downtown site or a low-voltage cabling crew pulling wire through finished office space — same form, same limits, same checklist.

That approach creates two problems. First, you’re over-insuring low-risk trades, which drives up their bid prices and makes your projects more expensive. A landscaping sub carrying a $10M umbrella because that’s what your template says is passing that premium cost straight through to you. Second — and this is the dangerous one — you’re under-insuring high-risk trades by not requiring the specialty coverages they actually need. A roofing sub with standard CGL but no hot work exclusion review, or a demolition sub without contractor’s pollution liability, can create exposure gaps that a standard template will never catch.

The Baseline: What Every Subcontractor Needs

Before we get into trade-specific requirements, here’s the minimum coverage that every sub on a commercial construction project should carry, regardless of trade:

| Coverage | Minimum Limits | Key Endorsements |

|---|---|---|

| Commercial General Liability | $1M per occurrence / $2M aggregate (occurrence-based) | CG 20 10, CG 20 37, CG 20 01, CG 24 04 — see endorsement guide |

| Workers’ Compensation | Statutory; EL $1M/$1M/$1M | Waiver of Subrogation in favor of GC |

| Commercial Auto | $1M combined single limit | Owned, hired, non-owned autos |

| Umbrella / Excess | $2M+ (follow form over CGL, auto, EL) | Additional insured on umbrella too |

Now let’s look at what changes by trade.

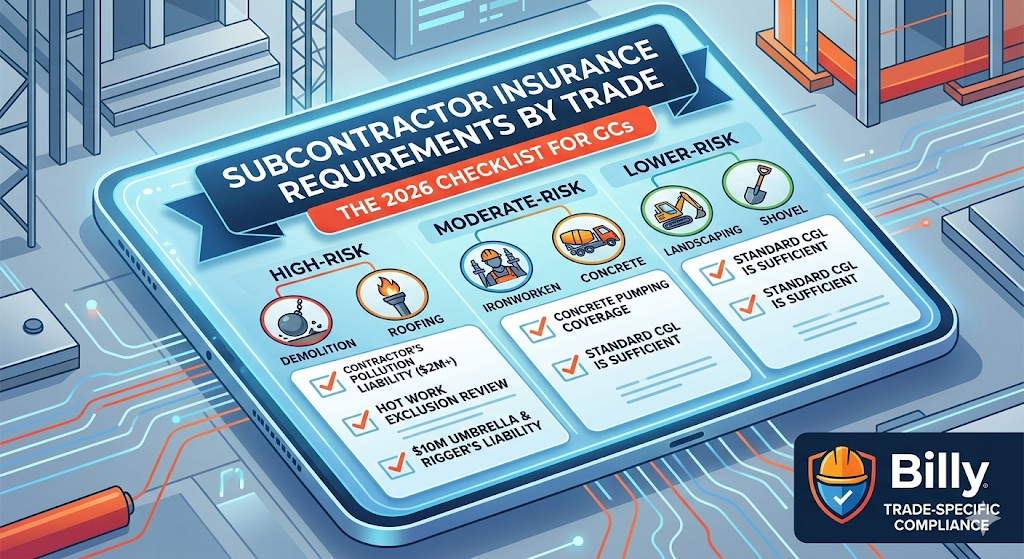

🔴 High-Risk Trades: Elevated Limits + Specialty Coverages

Demolition Contractors

| CGL | $2M per occurrence / $4M aggregate — double the baseline. Some GCs require $5M on urban projects. |

| Umbrella | $5M minimum. $10M on projects with adjacent occupied structures. |

| ⚠️ Specialty Required | Contractor’s Pollution Liability (CPL) — minimum $2M. Demolition disturbs asbestos, lead, PCBs. Standard CGL has absolute pollution exclusion. |

| Also verify | CGL doesn’t contain a “total pollution exclusion” (CG 21 49 or similar). Auto covers specialized hauling trucks. |

Roofing Contractors

| CGL | $2M per occurrence / $4M aggregate |

| Umbrella | $5M minimum |

| ⚠️ Critical Check | Hot work exclusion review — if the roofer uses torches, hot-applied bitumen, or welding, check CGL for hot work exclusions. Require removal or separate endorsement. |

| Completed Operations | Verify products-completed operations aggregate is separate from general aggregate. Confirm CG 20 37 covers full statute of repose period. |

Structural Steel / Ironworkers

| CGL | $2M per occurrence / $4M aggregate |

| Umbrella | $10M minimum. A single structural collapse can generate claims well into eight figures. The trend toward nuclear verdicts in construction makes this even more critical. |

| ⚠️ Specialty Required | Riggers’ liability / crane coverage — if the erector provides their own cranes, verify CGL and auto cover crane operations. Many standard policies exclude crane damage. |

| EMR threshold | Cap at 1.0 for steel erection — lower than the standard 1.25 threshold for other trades. |

Electrical Contractors

| CGL | $1M/$2M standard. Increase to $2M/$4M for high-voltage or industrial electrical. |

| Umbrella | $5M minimum. $10M on hospitals, data centers, mission-critical facilities. |

| ⚠️ If design-build | Professional Liability / E&O required when the electrical sub is responsible for design, engineering, or load calculations. $1M minimum. |

Mechanical / HVAC Contractors

| CGL | $1M/$2M standard. Increase to $2M/$4M for industrial process piping, boiler installation, or medical gas. |

| Umbrella | $5M minimum |

| ⚠️ Watch for | Refrigerant liability exclusion — some carriers exclude pollution from refrigerant releases on HVAC contractor policies. Also require Professional Liability if responsible for system design or commissioning. |

🟡 Moderate-Risk Trades: Standard Limits with Targeted Add-Ons

| Trade | CGL | Umbrella | Specialty / Watch For |

|---|---|---|---|

| Concrete / Masonry | $1M/$2M | $5M structural; $2M flatwork | Verify concrete pumping operations are covered — some carriers exclude or sublimit them. Auto should cover pump trucks. |

| Excavation / Earthwork | $1M/$2M | $5M minimum | ⚠️ Check for “subsurface operations exclusion.” Require CPL ($1M+) if any chance of encountering contaminated soil or USTs. |

| Plumbing | $1M/$2M standard; $2M/$4M for medical/fire suppression | $2M–$5M | Check for water damage sublimits — primary exposure for plumbing subs. Sublimit should equal per-occurrence limit. |

| Painting / Coatings | $1M/$2M | $2M | ⚠️ If any lead paint abatement on pre-1978 buildings, require dedicated pollution liability or lead paint endorsement. |

| Fire Protection / Sprinkler | $1M/$2M | $5M minimum | Completed operations coverage is critical — system failures years later can generate massive claims. Verify CG 20 37. Require Professional Liability if sub does hydraulic calcs. |

| Drywall / Interior Finish | $1M/$2M | $2M | Verify CGL doesn’t contain overly broad “care, custody, or control” exclusion for damage to building while working in it. |

🟢 Lower-Risk Trades: Standard Coverage Usually Sufficient

| Trade | CGL | Umbrella | Notes |

|---|---|---|---|

| Landscaping / Sitework | $1M/$2M | $1M–$2M | If applying chemicals, verify CGL or separate pollution policy covers herbicide/pesticide application damage. |

| Low-Voltage / Data Cabling | $1M/$2M | $1M–$2M | Data centers, hospitals, or classified facilities may require elevated limits + professional liability. Adjust by facility, not trade. |

| Flooring / Tile | $1M/$2M | $1M–$2M | VOC exposure from adhesives may trigger indoor air quality claims on occupied renovation projects — confirm CGL doesn’t exclude them. |

⚡ Specialty Contractors: Unique Requirements

Crane / Hoisting Operators

CGL: $2M/$4M minimum | Umbrella: $10M minimum

⚠️ Crane / rigging specific coverage required. Standard CGL often excludes crane operations. Require a separate crane liability policy or endorsement covering lifting operations, rigging, and load damage — minimum $5M. Verify mobile cranes are covered under auto (if highway-legal) or inland marine (if not). Coverage gaps between auto and CGL for mobile equipment are common and dangerous.

Environmental / Abatement Contractors

CGL: $1M/$2M | CPL: $5M/$5M (this is the primary coverage)

⚠️ Contractor’s Pollution Liability is the most important policy for this trade. The CGL’s absolute pollution exclusion means it provides almost no coverage for the work this sub actually performs. Also require Professional Liability if the contractor provides consulting, air monitoring, or clearance testing ($1M minimum).

Design-Build / Design-Assist Subcontractors

CGL: Standard per trade above | Professional Liability / E&O: $2M/$2M minimum

⚠️ Professional Liability is the critical coverage. Required for any sub providing design services, engineering, architectural work, or design-assist scope. On larger projects, $5M. Claims-made coverage is acceptable for professional liability (unlike CGL), but verify the retroactive date precedes the start of design services.

How to Implement Trade-Specific Requirements

Build requirement templates by trade classification.

Create a library of templates mapped to CSI divisions or trade categories. When you onboard a sub, assign the template that matches their scope. This is dramatically easier with a COI tracking platform that supports multiple requirement profiles.

Tie requirements to contract scope, not just trade name.

A “mechanical contractor” doing rooftop unit replacement has different risk than one installing medical gas piping. Adjust requirements based on the specific scope in the subcontract.

Review with your insurance broker annually.

Market conditions change. Carrier appetite shifts. New endorsement forms get introduced. Update your requirement templates at least once per year.

Use your tracking system to enforce it.

Billy’s AI Review Assistant verifies incoming certificates against your trade-specific templates automatically — catching limit shortfalls, missing endorsements, and expired coverages before the sub mobilizes. For complex or non-standard policies, Billy’s managed services team reviews documents within 24 hours.

🏗️ Stop Using One Template for Every Trade

Trade-specific requirement templates. Automated compliance verification. AI + human review. Connected to your full construction stack.

Request a Free Demo →📚 Related Resources

|

Guide Insurance Endorsements: CG 20 10, CG 20 37 & Primary Noncontributory → |

Guide Certificate Holder vs Additional Insured: What GCs Must Verify → |

|

Industry Trends Nuclear Verdicts Are Rewriting Construction Insurance Rules → |

Free Tool |

|

Compliance Hub |

Comparison |