A general contractor running 40 active projects with 200+ subcontractors on each is managing tens of thousands of insurance documents at any given time. Every one of those certificates carries specific endorsement requirements, coverage thresholds, and expiration dates that shift with each contract. When one lapses or one waiver of subrogation is missing, the GC holds the exposure. Software designed for healthcare vendor management or fleet logistics does not account for the endorsement complexity, warranty tail risk, or subcontractor volume that define construction insurance compliance.

Billy was built exclusively for construction. The AI Review Assistant reads certificates at the endorsement level, checking for provisions like CG2010 additional insured status, waiver of subrogation, and cancellation notice requirements. With 100,000+ policies tracked across 3,500+ projects, Billy handles COI compliance at the scale construction demands.

What Is COI Compliance Software?

Certificate of insurance (COI) compliance software automates the collection, review, storage, and monitoring of insurance documents from vendors and subcontractors. In construction, the requirements go deeper than confirming a policy exists. The software must verify specific endorsements, track policy types, flag gaps in coverage limits, and monitor renewals across every subcontractor on every project.

For risk managers and compliance teams, COI tracking software replaces the spreadsheets, email chains, and phone calls that traditionally consumed hours each week. For subcontractors, it reduces the back-and-forth of sending updated certificates to multiple GCs.

The Problem with Manual COI Tracking in Construction

Construction firms are adopting digital tools faster than at any point in the industry’s history. A 2023 Deloitte study found that construction businesses increased technology adoption by 20%, with the average company now using 6.2 digital tools compared to 5.3 the prior year. COI tracking, though, remains one of the last workflows still stuck in email and Excel at many firms.

When you manage hundreds of subcontractors across multiple projects, one missed renewal can shut down a job site or expose the GC to uninsured liability. Manual processes break down because they depend on a compliance coordinator remembering to follow up, an agent responding promptly, and someone reading the certificate closely enough to catch that a scheduled waiver of subrogation names the wrong project.

Endorsement-level verification is where most manual workflows fail entirely. A compliance team member scanning a COI can confirm that general liability coverage meets the $1M/$2M threshold. That same person is far less likely to catch that a CG2010 endorsement has not been confirmed in the underlying policy, or that a claims-made professional liability policy expired three months ago without tail coverage.

What Construction Insurance Verification Actually Requires

A COI is a summary document. It confirms coverage exists, lists policy numbers and limits, and names certificate holders. Construction contracts typically require specific endorsements, particular policy structures, and coverage provisions that can only be confirmed by reviewing the underlying policy documents or endorsement schedules, not the COI alone.

Construction-specific insurance verification requires checking four categories of requirements that horizontal compliance platforms routinely miss or handle superficially.

Waiver of Subrogation

A waiver of subrogation is a contractual provision that prevents an insurer from pursuing a third party to recover money paid on a claim. In construction, GCs require subcontractors to carry this waiver so that if a loss occurs, the subcontractor’s insurer cannot sue the GC to recoup its payout.

Two types exist: blanket and scheduled. A blanket waiver applies to all parties the insured has agreed to waive subrogation rights against. A scheduled waiver names specific parties. GCs generally prefer blanket waivers because they do not require the GC to be individually listed.

The critical detail: a waiver of subrogation must be verified at the endorsement level, not inferred from the certificate face page. The COI may reference general liability coverage without indicating whether the waiver endorsement is actually attached to the policy.

Claims-Made vs. Occurrence Policies

Occurrence-based policies cover any incident that happens during the policy period, regardless of when the claim is filed. If a subcontractor’s general liability policy was active during the 2024 project year and a bodily injury claim surfaces in 2027, occurrence coverage responds.

Claims-made policies cover claims filed during the active policy period. If the same subcontractor’s professional liability policy lapses in 2025 and the claim arrives in 2027, there is no coverage unless the subcontractor purchased tail coverage (an extended reporting period endorsement).

On long-duration construction projects, claims-made policies create significant tail risk. A defect discovered years after project completion may have no coverage if the subcontractor let a claims-made policy lapse. Billy tracks both the policy type and the expiration date, alerting compliance teams when a claims-made policy is approaching lapse on a project with ongoing exposure.

What Is Indemnity?

Indemnity is a contractual obligation for one party to compensate another for losses, damages, or liabilities. In construction subcontracts, indemnity clauses typically require the subcontractor to hold the GC harmless from claims arising out of the subcontractor’s work.

Three forms appear in construction contracts. Broad form indemnity requires the subcontractor to cover losses even if the GC is partially at fault (prohibited in many states). Intermediate form covers the subcontractor’s negligence and any shared fault, but not the GC’s sole negligence. Limited (or comparative) form covers losses only to the extent of the subcontractor’s own negligence.

The connection to COI compliance is direct: an indemnity clause is only as strong as the insurance backing it. If a subcontractor agrees to broad form indemnity but carries insufficient general liability limits or lacks an umbrella policy, the GC is left holding an unenforceable promise. Billy’s compliance checks verify that coverage limits and policy types on the COI match the indemnity obligations in the subcontract.

Additional Insured Endorsements

Most construction contracts require the GC to be named as an additional insured on the subcontractor’s liability policies. The standard endorsement is the CG2010 (or CG2037 for completed operations), which extends the subcontractor’s coverage to the GC for claims arising out of the subcontractor’s work.

A common compliance failure: the COI lists the GC as the certificate holder, and the compliance team assumes additional insured status is included. Certificate holder and additional insured are different designations. Additional insured status requires a specific endorsement attached to the underlying policy. The CG2010 form must be confirmed in the endorsement schedule or policy documents; its presence cannot be assumed from the certificate holder field or the COI face page alone.

How Billy Automates the Full Verification Workflow

Billy handles the complete COI compliance cycle: collection, AI-powered review, compliance verification, deficiency resolution, and ongoing monitoring. Every step is built around construction contract requirements, subcontractor workflows, and the endorsement-level detail that construction insurance demands.

Automated COI Collection

Billy sends automated requests to subcontractors and their insurance agents, collecting certificates and endorsement documents without manual email correspondence. Subcontractors upload documents directly into Billy, where they are parsed and matched to the correct project and contract requirements.

The Insurance Wallet gives subcontractors a central place to store and share their own COIs across multiple GCs. Instead of fielding separate requests from every general contractor on every project, a subcontractor maintains one updated set of documents and grants access as needed.

AI-Powered Document Review

Billy’s AI Review Assistant goes beyond conventional OCR extraction of policy numbers and coverage limits. The system identifies specific endorsements (CG2010, CG2037, waiver of subrogation, cancellation notice provisions) within the actual policy and endorsement documents, then verifies them against the contract requirements for each project. This endorsement-level review is the core differentiator: Billy confirms coverage provisions exist in the underlying policy, not just on the certificate face page.

The 48-hour review SLA means compliance teams receive flagged deficiencies within two business days, compared to the approximately seven-day turnaround typical of manual review. That difference matters when a subcontractor needs to be cleared before mobilizing on Monday.

Subcontractor Prequalification

COI compliance is a verification step that happens after a subcontractor is selected. Prequalification is the step before, where you assess whether a subcontractor meets your safety, financial, and insurance standards before they bid.

Billy includes a Subcontractor Prequalification Tool as an integrated product, not an add-on or third-party connection. Prequalification data feeds directly into the COI compliance workflow, so when a subcontractor passes prequal and is awarded work, their insurance requirements are already loaded and tracking begins immediately. Prequalification is uncommon among general-purpose COI platforms, which typically require construction teams to manage a separate system for that step.

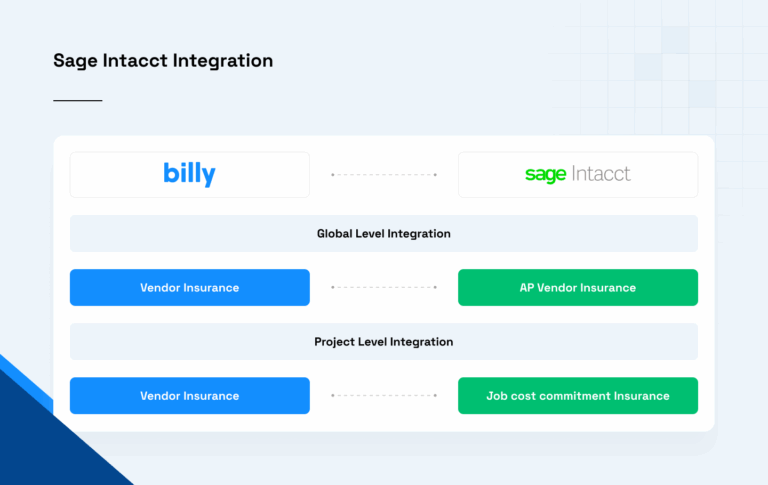

Procore and ERP Integrations

Billy integrates with the project management and accounting platforms construction teams already use: Procore, Autodesk, CMiC, Sage 300, Sage Intacct, JD Edwards, Viewpoint Vista, Acumatica, and DocuSign. When a subcontractor is added to a project in Procore, Billy can automatically initiate the COI collection and compliance workflow without duplicate data entry.

These integrations keep subcontractor records, project assignments, and compliance statuses synchronized across systems. A compliance manager can confirm whether a subcontractor is cleared to work on a given project without toggling between platforms.

Post-Project Warranty Tracking

Project close-out does not end insurance exposure. In California, for example, construction defect statutes allow claims up to 10 years after completion for latent defects. Other states carry 5 to 7 year windows.

Billy tracks subcontractor insurance beyond project completion, monitoring policy renewals and coverage continuity during the warranty exposure period. If a subcontractor’s general liability policy lapses two years after a project closes, Billy flags the gap. Many COI tracking systems stop monitoring at project close, a common gap that leaves GCs exposed during the highest-risk window for latent defect claims.

Who Uses Billy

General contractors managing hundreds of subcontractors across multiple active projects use Billy to automate the collection, review, and monitoring of COIs. The charge-back model allows builders to pass COI compliance costs to subcontractors, keeping overhead predictable as project volume scales.

Brokers and carriers managing compliance on behalf of their construction clients use Billy to centralize document collection and reduce the back-and-forth between agents, subcontractors, and GC compliance teams.

Subcontractors use the Insurance Wallet to store their certificates, endorsements, and policy documents in one location. When a new GC requests proof of coverage, the subcontractor shares access rather than generating a new certificate request through their agent.

Why Construction-Specific Software Outperforms Horizontal Platforms

Horizontal COI tracking platforms serve property management, healthcare, transportation, and manufacturing alongside construction. Their compliance rules, document review logic, and workflows must accommodate every industry’s requirements, which means construction-specific needs like warranty tail tracking and integrated prequalification are either absent or handled through workarounds.

A construction-exclusive platform carries a different set of defaults. Billy’s compliance templates are built around the endorsements GCs actually require: CG2010, CG2037, waiver of subrogation (blanket and scheduled), and cancellation notice provisions as specified by policy terms and state requirements. The prequalification tool lives in the same workflow as COI tracking. Warranty monitoring extends for 5 to 10 years after project close. The integrations connect to Procore, CMiC, and Sage, not Salesforce or ServiceNow.

The 48-hour review SLA reflects a staffing and process model tuned for construction document volume. When your compliance team needs a subcontractor cleared before they mobilize on Monday, a seven-day review cycle is not workable.

FAQ

What is a waiver of subrogation in construction?

A waiver of subrogation is an endorsement that prevents a subcontractor’s insurer from suing the GC to recover money paid on a claim. GCs require this waiver in subcontracts so that after a covered loss, the insurer absorbs the cost rather than pursuing the general contractor. Waivers can be blanket (applying to all parties) or scheduled (naming specific parties).

What is the difference between claims-made and occurrence insurance?

Occurrence policies cover incidents that happen during the policy period, no matter when the claim is filed. Claims-made policies only cover claims filed while the policy is active, meaning a lapsed claims-made policy provides no coverage for later-discovered issues unless tail coverage (an extended reporting period) was purchased.

What does indemnity mean in a construction contract?

Indemnity is a contractual obligation requiring one party to compensate another for specified losses or liabilities. In construction, subcontractors typically agree to indemnify the GC against claims arising from the subcontractor’s work. The indemnity clause is only enforceable if the subcontractor carries sufficient insurance to back it.

What is subrogation meaning in insurance?

Subrogation is the right of an insurer, after paying a claim, to pursue recovery from a third party responsible for the loss. In construction, this means a subcontractor’s insurer could sue the GC to recoup claim payments, which is why GCs require waivers of subrogation as a standard contract provision.

What should COI compliance software check beyond coverage limits?

Effective COI compliance software should verify specific endorsements (such as CG2010 additional insured and waiver of subrogation), distinguish between claims-made and occurrence policy types, confirm that coverage provisions match subcontract requirements, and track cancellation notice obligations. Checking only dollar limits misses the endorsement-level gaps where most compliance failures occur.

How long should subcontractor insurance be tracked after project completion?

Subcontractor insurance should be monitored through the full statute of limitations for construction defect claims in the relevant jurisdiction. Depending on the state, this window ranges from 5 to 10 years after project completion. Latent defects discovered years later can leave the GC exposed if the subcontractor’s coverage lapsed without anyone tracking it.

Get Started

Construction COI compliance requires endorsement-level document review, not just coverage limit checks. It requires tracking that extends years past project close-out, and it requires a workflow that connects prequalification, insurance verification, and project management in one system. Billy delivers all three, with AI-powered review tuned specifically for construction endorsements, integrated subcontractor prequalification, and warranty-period monitoring that keeps running long after the last punch list item is closed.

Request a Billy demo to see endorsement-level AI review, subcontractor prequalification, and post-project warranty tracking in your own workflow.

If you are still building your compliance process, download Billy’s free COI tracking template or the 2026 audit-ready checklist to benchmark your current coverage gaps before evaluating software.