The Question Every Risk Manager Eventually Asks

“Can your AI identify equivalent forms?”

It’s one of the most common questions we hear from general contractors evaluating Billy. And it makes perfect sense—if a subcontractor’s carrier submits their proprietary form instead of the standard CG2010 Additional Insured endorsement you require, you need to know whether it provides equivalent coverage.

The short answer? AI alone can’t reliably solve this problem. But that doesn’t mean you’re stuck manually reviewing every non-standard form. Here’s why this is more complex than it appears, and how Billy’s managed service team provides a better solution than automation alone.

What Are “Equivalent Forms” in Construction Insurance?

In an ideal world, every certificate of insurance would include the exact endorsements your contract requires: CG2010, CG2037, CG2503, etc. But in practice, insurance carriers often substitute their own proprietary forms that claim to provide “equivalent” coverage.

Common examples include:

- Liberty Mutual’s CG D3 65 04 12 (their version of additional insured coverage)

- Travelers’ proprietary waiver of subrogation forms

- Carrier-specific umbrella/excess liability endorsements

- Manuscript endorsements with custom language

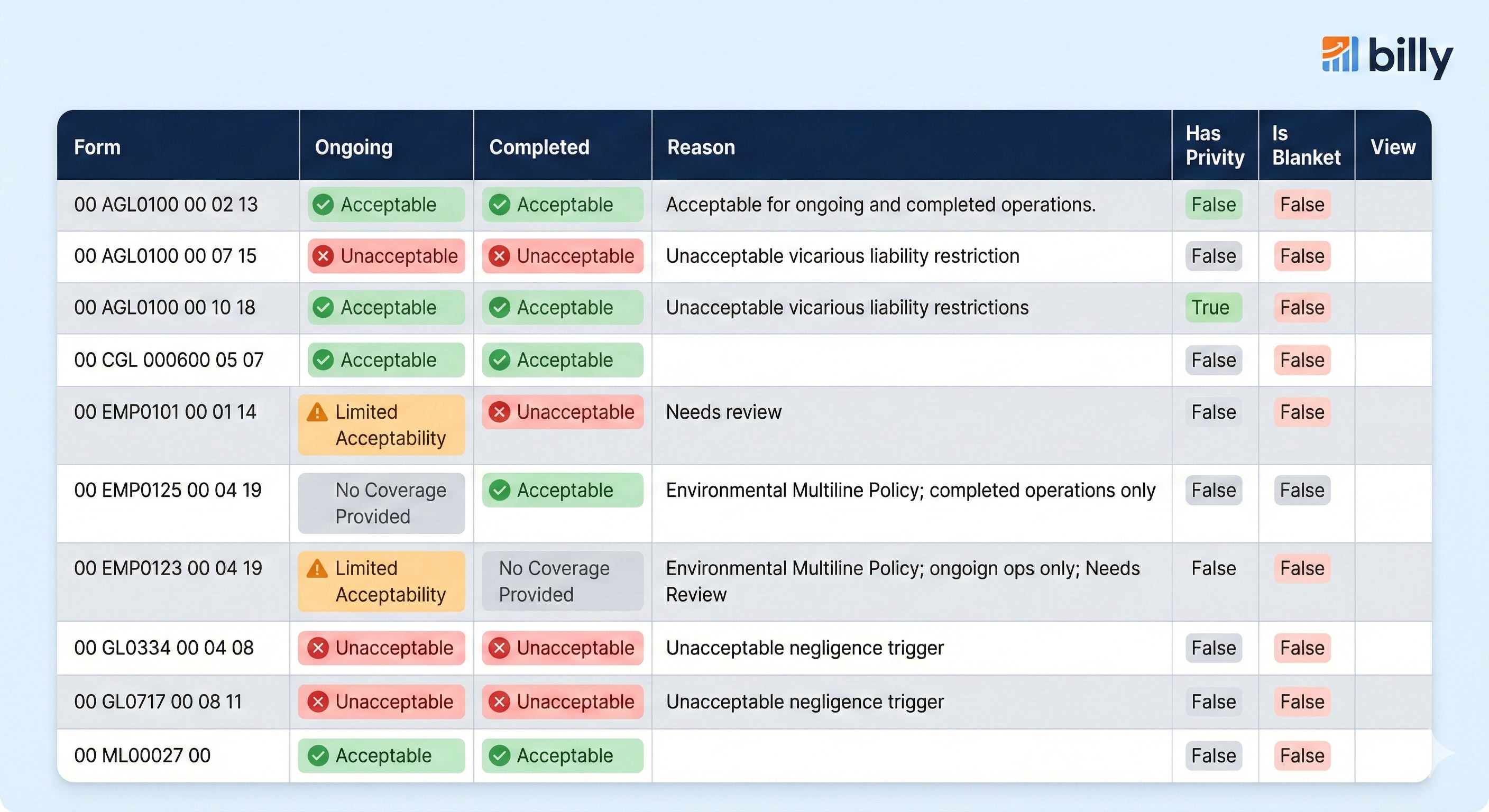

The critical question: Does this proprietary form actually provide the same protection as the standard ISO form your contract requires?

Why AI Can’t Reliably Identify Equivalent Forms

You might assume this is a perfect problem for AI to solve—just train a model to recognize equivalent language across different forms. But there’s a fundamental challenge: there is no single “ground truth” to train on.

Here’s why:

1. No Universal Standard for “Equivalence”

Unlike identifying a standard CG2010 form (which has consistent form numbers and language), determining whether a proprietary form is “equivalent” requires legal interpretation. Two experienced insurance professionals might disagree on whether a carrier’s custom endorsement provides adequate coverage.

2. Context Matters

Whether a form is acceptable depends on:

- Your specific contract language

- The scope of work

- State-specific insurance regulations

- Your company’s risk tolerance

- The subcontractor’s tier level

A form that’s acceptable for a small painting subcontractor on a low-risk tenant improvement might be inadequate for a structural steel contractor on a $50M project.

3. Coverage Gaps Are Subtle

The difference between adequate and inadequate coverage often comes down to nuanced language differences:

- Does the form cover ongoing operations AND completed operations?

- Is coverage triggered by an “occurrence” or “claim”?

- Are there silent exclusions buried in the fine print?

- Does the waiver of subrogation apply to all parties in your contract?

AI can identify similar-looking language, but it cannot assess whether subtle differences create material coverage gaps.

The Real Risk: False Confidence

Here’s what concerns us most about relying solely on AI for equivalent form review: false positives create false confidence. If an AI flags a proprietary form as “equivalent” when it actually contains gaps, you’ve unknowingly accepted inferior coverage. You won’t discover the problem until you have a claim—and by then, it’s too late.

Billy’s Solution: Expert Human Review Where It Matters

This is exactly where Billy’s Managed Service offering provides value that automation alone cannot.

How It Works:

- AI handles routine checks : Our AI reviews every COI for standard compliance issues, including expired dates, incorrect certificate holders, missing endorsements, incorrect limits, etc.

- CRIS Certified Experts review nuanced cases: when a non-standard or proprietary form is submitted, it’s flagged for review by our managed service team—insurance professionals who understand the legal implications of coverage language.

- You get a definitive answer: Rather than a probabilistic AI assessment, you receive a clear determination: “This form is acceptable” or “This form has the following gaps and needs to be replaced.”

Real-World Example:

A subcontractor submits a Liberty Mutual policy with form CG D3 65 04 12 instead of the required CG2010. Our managed service team:

- Compares the proprietary form language to CG2010

- Identifies that it covers ongoing operations but excludes completed operations for structural work

- Flags the gap and requests the appropriate endorsement

- Documents the resolution in your Billy account

Without expert review, this coverage gap might have gone unnoticed until a post-completion claim arose.

Why This Matters for Your Compliance Program

If you’re a GC managing hundreds of subcontractors, you can’t afford to have your team manually reviewing every non-standard form. But you also can’t afford to blindly accept them.

The Billy approach gives you the best of both worlds:

- Automation handles 80%+ of routine compliance checks

- Expert review handles the 20% of nuanced cases that require human judgment

- You maintain defensible compliance without drowning your team in paperwork

The Bottom Line

Can AI identify equivalent insurance forms? Not reliably—and anyone telling you otherwise is overselling their technology.

But that doesn’t mean you’re stuck with manual review. Billy’s managed service team provides expert-level review for the complex cases that matter, while our AI handles the routine compliance checks at scale.

The result: Faster processing, stronger compliance, and protection against the coverage gaps that create real financial risk.

Want to see how Billy handles non-standard forms in your compliance workflow? Request a demo to see our managed service in action.