Construction projects are inherently complex, involving multiple stakeholders such as contractors, subcontractors, suppliers, and property owners. Each project carries unique risks, including financial, legal, environmental, and safety concerns. Without proper risk management strategies in place, businesses may face costly claims, project delays, or even legal disputes.

Managing Risk in Construction Projects

One of the most effective ways to mitigate risk is through well-structured insurance coverage. However, ensuring adequate protection requires a collaborative effort between builders, insurance brokers, and carriers. By working together, these entities can streamline compliance, enhance financial security, and foster long-term business success. A construction risk insurance specialist plays a crucial role in this collaboration, ensuring that all parties are adequately protected against potential liabilities.

Understanding Risk Transfer in Construction

Risk transfer is a fundamental concept in construction risk management. It involves shifting the financial responsibility of potential losses from one party to another, typically through contracts and insurance policies. Effective risk transfer strategies help construction businesses protect their assets, reduce liability exposure, and ensure project continuity.

Common Methods of Risk Transfer

- Well-Defined Contracts: Every construction contract should clearly define the responsibilities of all parties involved. This includes indemnification clauses, hold harmless agreements, and warranties that specify who is accountable for potential risks.

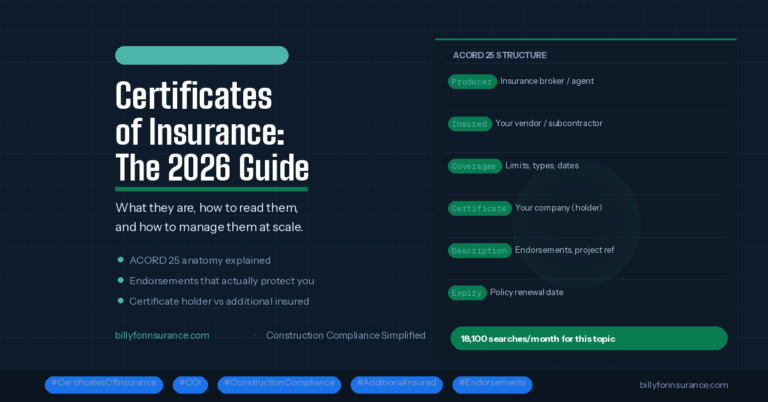

- Comprehensive Insurance Requirements: Builders should require vendors and subcontractors to provide Certificates of Insurance (COIs), additional insured endorsements, and waivers of subrogation. These endorsements help safeguard against financial losses resulting from third-party negligence.

- Surety Bonds: Surety bonds act as a financial guarantee that contractors and subcontractors will fulfill their contractual obligations. They provide protection against project delays and non-performance.

By implementing these risk transfer measures, builders can minimize financial uncertainty and ensure smoother project execution.

The Cost of Overlooking Risk Management

Failure to implement proper risk management strategies can lead to significant financial losses.

Consider the following real-world scenario:

A builder hired a flooring subcontractor to resolve an ongoing issue with a newly installed surface. The subcontractor applied a chemical solution to fix the problem, but the solution inadvertently corroded nearby metal surfaces, damaging HVAC components, furniture, and appliances.

Unfortunately, the builder’s contract only required the subcontractor to carry general liability insurance. Since pollution-related incidents were not covered under the policy, the claim was denied. As a result, the builder had to pay $190,000 out-of-pocket to cover repair costs, suffered an increase in insurance premiums, and faced reputational damage.

This scenario underscores the importance of establishing comprehensive insurance requirements and working closely with brokers to ensure all potential risks are accounted for in policy coverage. Engaging a construction risk insurance specialist can help builders proactively address coverage gaps and mitigate costly exposures.

The Role of Insurance Brokers in Construction Risk Management

The U.S. construction insurance market is valued at over $53 billion, with most policies purchased through insurance brokers. Brokers serve as intermediaries between construction businesses and insurance carriers, helping builders navigate complex policy terms and secure adequate coverage.

How Brokers Add Value

- Risk Assessment: Insurance brokers analyze construction operations to identify potential risks and recommend appropriate coverage options.

- Policy Customization: Brokers tailor insurance policies to align with the specific needs of a project, ensuring that all potential exposures are covered.

- Claims Advocacy: In the event of a claim, brokers assist builders in navigating the claims process, maximizing recovery, and minimizing financial impact.

- Cost Management: By negotiating competitive premiums and recommending risk mitigation strategies, brokers help construction businesses control insurance costs.

With rising insurance costs and increasing regulatory requirements, construction companies that proactively engage with brokers are better positioned to manage risk effectively.

The Impact of Rising Insurance Costs on Construction Budgets

Insurance costs are a significant component of a construction project’s overall budget. On average, insurance expenses account for 3% to 10% of total project costs. For a $5 million project, this translates to insurance costs ranging from $150,000 to $500,000.

Additionally, the construction industry has seen an annual increase in insurance premiums of approximately 4.6%. Factors contributing to these rising costs include:

- Increased frequency and severity of claims

- Rising material and labor costs

- Stricter regulatory requirements

- Higher litigation expenses

Without proper risk management and compliance strategies, construction businesses may struggle to absorb these rising costs, ultimately affecting their profitability.

Leveraging Technology for Compliance and Risk Management

In recent years, new technology and software has played a transformative role in simplifying compliance and improving risk management in the construction industry. Digital platforms and automation tools are streamlining insurance tracking, reducing administrative burdens, and enhancing collaboration among stakeholders.

Benefits of Technology in Construction Compliance

Centralized Data Management: Digital compliance platforms provide a centralized repository for insurance documents, COIs, and policy details, making it easier for construction teams to track compliance in real-time.

Automated Policy Monitoring: Advanced software solutions send automated alerts for insurance policy renewals, helping businesses avoid lapses in coverage.

Improved Collaboration: Cloud-based platforms enable builders, brokers, and insurers to access and update compliance records in real-time, ensuring transparency and accountability.

By embracing technology, construction businesses can reduce human error, minimize compliance risks, and allocate resources more effectively.

The Future of Compliance: Automation in Risk Management

Automation is revolutionizing the way construction businesses manage risk and insurance compliance. By leveraging AI and machine learning, companies can optimize processes, improve accuracy, and enhance operational efficiency.

Key Advantages of Automation

- Enhanced Accuracy: Automated compliance systems reduce the risk of human error, ensuring that insurance policies meet project requirements.

- Time Efficiency: Manual insurance tracking can be time-consuming. Automation streamlines data collection, verification, and reporting.

- Cost Savings: By reducing administrative workload and minimizing compliance violations, automation helps construction businesses lower operational costs.

Incorporating automation into compliance processes allows builders to focus on strategic initiatives rather than administrative tasks, ultimately improving business performance.

Strengthening Risk Management in Construction

Navigating the complexities of construction insurance requires a proactive approach to risk management. Builders, brokers, and insurance carriers must work together to develop comprehensive strategies that protect businesses from financial and legal exposure.

Key Takeaways for Builders:

- Establish clear insurance requirements in all contracts.

- Collaborate with brokers to identify potential risk gaps and secure adequate coverage.

- Leverage technology to automate compliance tracking and minimize human error.

- Stay informed about evolving insurance regulations and industry best practices.

By prioritizing risk management and embracing innovative solutions, construction professionals can enhance project security, reduce costs, and foster stronger industry partnerships. With the right approach to compliance and risk management, builders can confidently navigate the complexities of the construction industry while protecting their bottom line.

Frequently Asked Questions

A CRIS (Construction Risk and Insurance Specialist) certification is a designation for insurance professionals specializing in construction risk management. It demonstrates expertise in industry-specific insurance policies, risk transfer strategies, and compliance best practices.

Builder’s risk insurance covers property damage during construction due to risks like fire, theft, vandalism, and weather events. It typically includes coverage for materials, equipment, and structures under construction but excludes liability and worker injuries.

General contractors, property owners, developers, and subcontractors often purchase builder’s risk insurance to protect their investment in a construction project. It is usually required by lenders and contract agreements.