General contractors can no longer avoid the maze of insurance requirements and compliances. Misunderstanding insurance requirements can incur costs in the tens-of-thousands to millions of dollars.

On an average day, a general contractor handles projects worth millions, makes decisions that impact hundreds of workers, and signs contracts studded with legal jargon. It’s a lot to keep track of.

Fear not, this guide will be your step-by-step companion into contractor insurance, highlighting the pitfalls that could save you money, reputation, and frustrations.

A Step-by-Step Guide to Navigating Insurance Requirements for General Contractors

Step 1: Understanding Essential Insurance Policies for General Contractors

General contractors are exposed to numerous risks, from property damage to injuries and product liabilities. Hence, understanding crucial insurance policies becomes imperative, more than a mere compliance requirement.

- General Liability Insurance: This coverage protects you from financial loss arising from bodily injuries, property damage, advertising injuries, and others happening on the job.

- Workers’ Compensation Insurance: As a general contractor, this coverage is fundamental to handling medical expenses and wage replacement if an employee suffers work-related injuries.

Insurance is the protective backbone for general contractors. It assists in covering financial deficits derived from unexpected damages, medical expenses related to worker injuries, and defending claims or lawsuits from unsatisfied clients. The insurance policy acts as a safety net, allowing the business to continue to function smoothly even in adverse situations.

Step 2: Obtain and Compare Quotes from Multiple Insurers

Securing the right insurance coverage at a competitive price requires diligent research and comparison. This approach helps you gather a variety of quotes and ensures you are not limited to one perspective or pricing model.

Key actions to take:

- Research and Contact Multiple Providers: Identiry and contact a diverse set of insurance companies and brokers to request quotes. Ensure these providers have experience in insuring general contractors.

- Evaluate Policy Details: Thoroughly compare each quote, looking beyond just the premium cost. Pay close attention to policy limits, deductibles, exclusions, and any additional coverages or endorsements.

- Tailor Coverage to Specific Needs: Customize your insurance coverage to fit the specific risks associated with your projects and business operations. Consider endorsements or riders that address unique risks you face.

By taking these steps, you can ensure that you obtain the most comprehensive and cost-effective insurance coverage tailored to your specific needs as a general contractor. Doing this helps in mitigating risks and protecting your business against potential liabilities.

Step 3: Evaluating Construction Business Insurance Needs

Your construction business insurance needs are gleaned from various factors, including the nature of the projects you handle, the types of risks involved, the size of your operations, and the specific regulatory requirements in your business locality.

There’s no one-size-fits-all insurance policy, as different construction businesses will have unique risk profiles and corresponding insurance needs. It’s crucial to review these needs regularly as your operations scale or diversify.

Expert advice from an insurance agent who understands the contracting business can be invaluable.

With a solid understanding of essential insurance policies, the audit process, and your construction business’s unique insurance needs, you’re now better equipped to navigate insurance requirements as a general contractor.

Implementing Insurance Requirements in Contracts

Vague or generic contract language can leave room for interpretation and potentially lead to costly disputes. Therefore, clearly defined contract clauses relating to insurance requirements should be a top priority.

Understanding general contractor license requirements and confidently implementing insurance terms in your contracts will not only ensure the legality of your operations but also improve your reputation and client relationships. Compliance with insurance requirements is critical for the smooth running of your business and avoiding potential legal troubles.

Streamlining compliance can be accomplished through consistent record-keeping, regular license and insurance reviews, and an inherent commitment to understanding the evolving landscape of contractor insurance and licensing requirements. Robust compliance practices translate to a more reliable, prepared, and prosperous business.

A compliance management system will assist in maintaining up-to-date records and conducting regular reviews.

Remember, building an informed, compliant contracting business is not only about ticking boxes – it’s about establishing a credible reputation and confidence in your processes, fostering strong client relationships, and mitigating risks.

Risks of Non-Compliance with Insurance Requirements

Not adhering to the regulations and not having adequate insurance coverage can lead to severe consequences.

Firstly, it opens the door to potential lawsuits from clients, third-party members, or employees, which could impact companies from both a financial and reputational standpoint.

Beyond fines and legal action, noncompliance can negatively impact a contractor’s business in terms of missed job opportunities. Many clients may refuse to do business with contractors who fail to meet insurance requirements, viewing it as a significant risk.

Here are two critical ways in which noncompliance impacts a general contractor’s ability to secure and maintain business:

1. Securing Business from Owners/Developers

Owners and developers prioritize working with contractors who meet all regulatory and insurance requirements. Noncompliant contractors are often viewed as high-risk, which can deter potential clients from awarding them contracts.

2. Hiring Compliant Subcontractors

General contractors rely on subcontractors to complete various aspects of a project. Ensuring subcontractors comply with insurance requirements is crucial for risk mitigation, avoiding project interruptions, and maintaining trust that leads to positive referrals.

In summary, compliance with insurance requirements is vital for general contractors to secure business from owners and developers and to manage risk effectively when hiring subcontractors. Noncompliance not only limits opportunities but also undermines the overall stability and reputation of the contracting business.

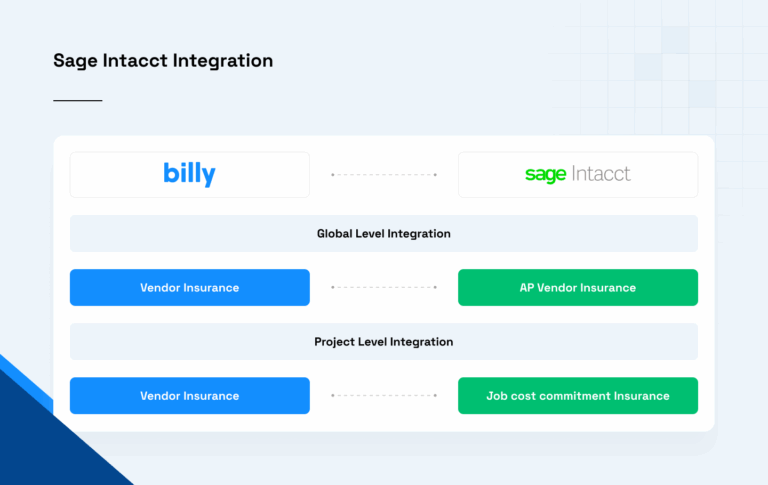

Making Insurance Requirements Work for You with the Billy Platform

Understanding the insurance needs of general contractors, from workers’ compensation to general liability, sends you on the right path. Remember, it’s all about maintaining financial stability, assuring clients, and mitigating risks, both unpredictable and inevitable.

Find out how Billy can simplify and improve your insurance compliance process. Request a demo today!

Frequently Asked Questions

Is it important for a contractor to be insured?

Yes, contractors must be insured. Insurance provides protection against various risks, such as property damage, injuries, or accidents that may occur during construction projects. Without insurance, contractors could face significant financial liabilities and legal consequences. Being insured not only safeguards the contractor’s business but also provides peace of mind to clients, demonstrating professionalism and responsibility in the construction industry.

What does “fully insured” mean for contractors?

“Fully insured” means that contractors have obtained comprehensive insurance coverage that meets all necessary requirements. This typically includes liability insurance, worker’s compensation insurance, and possibly other specific types of coverage, depending on the nature of the work. Being “fully insured” ensures that contractors are adequately protected against potential risks and liabilities that may arise during their projects.

What’s the difference between being bonded and insured?

Being bonded and insured serve different purposes for General Contractors (GCs). Insurance protects against financial losses resulting from accidents or damages during a project, while bonding ensures that the GC will fulfill contractual obligations and compensate for any breaches. Essentially, insurance covers unforeseen events, while bonding provides a guarantee of performance and financial security to clients.