CG 20 10 is the most requested insurance endorsement in construction. GCs require it from every sub, owners require it from every GC — yet most compliance teams still accept COIs without confirming the endorsement is actually attached. Here’s what CG 20 10 is, what it covers, what it doesn’t, and exactly how to verify your subs have it.

If you’ve ever sent a subcontractor a contract that says “provide Additional Insured status via CG 20 10 endorsement” — and then accepted their COI without checking whether the endorsement was actually attached — you’ve accepted a false sense of security in place of real risk transfer.

CG 20 10 is not automatically included in a general liability policy. It has to be added as an endorsement. A COI that lists you as a certificate holder does not make you an Additional Insured. Only the endorsement does that.

What Is CG 20 10?

CG 20 10 is an ISO (Insurance Services Office) standard endorsement form officially titled “Additional Insured – Owners, Lessees or Contractors – Scheduled Person or Organization.” It attaches to a subcontractor’s Commercial General Liability (CGL) policy and adds the general contractor (or property owner or developer) as an additional insured on that policy.

There are several editions of CG 20 10. The most current is the CG 20 10 04 13 (April 2013 edition). Older editions — 10/01 and 07/04 — have different coverage scopes, and the 04/13 edition narrows coverage in ways that matter for GCs. Always confirm the edition date when reviewing endorsements.

What CG 20 10 Covers — and What It Doesn’t

What it covers

Third-party bodily injury and property damage claims arising from the sub’s ongoing operations where both the sub and GC may be liable.

What it doesn’t cover

The GC’s sole negligence. Claims after the sub’s work is complete. Professional errors or design liability. Claims exceeding the sub’s policy limits.

Key coverage limitations of CG 20 10 04/13

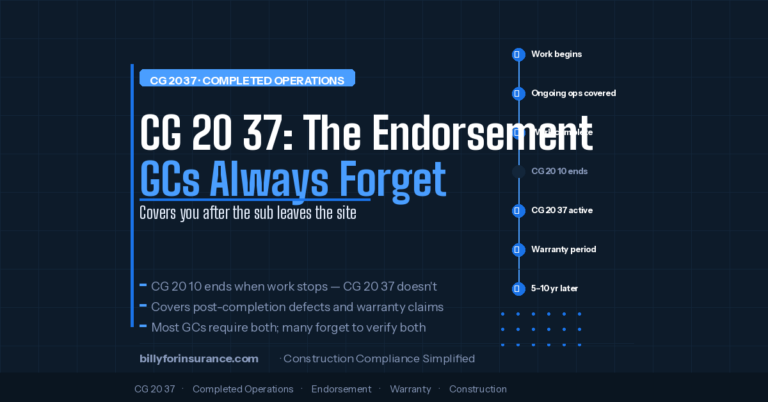

- Ongoing operations only: Coverage ends when the subcontractor’s work on that project is complete. For post-completion protection, you need CG 20 37 — they must be required together

- Proportional liability: The 04/13 edition limits coverage to situations where the sub is at least partially at fault. If the GC is 100% responsible for a loss, the sub’s policy may not respond

- No coverage for GC’s sole negligence: A subcontractor cannot insure the GC against the GC’s own errors

- State variations: Some states restrict or prohibit certain indemnity provisions, which can affect how CG 20 10 applies. Verify coverage requirements are enforceable in the project’s jurisdiction

Blanket vs. Scheduled Additional Insured: The Difference That Matters

There are two ways a sub’s policy can provide Additional Insured status: scheduled and blanket.

| Type | How it works | GC’s risk |

|---|---|---|

| Scheduled (specific) | Your company name is listed explicitly on the endorsement form. Coverage is unambiguous. | Lower — clear documentation |

| Blanket | Coverage extends to anyone the sub is required by written contract to add as AI. Doesn’t list you by name. | Medium — depends on contract language |

| No endorsement | COI lists you as certificate holder only. No AI status provided despite what the COI says. | High — no actual coverage |

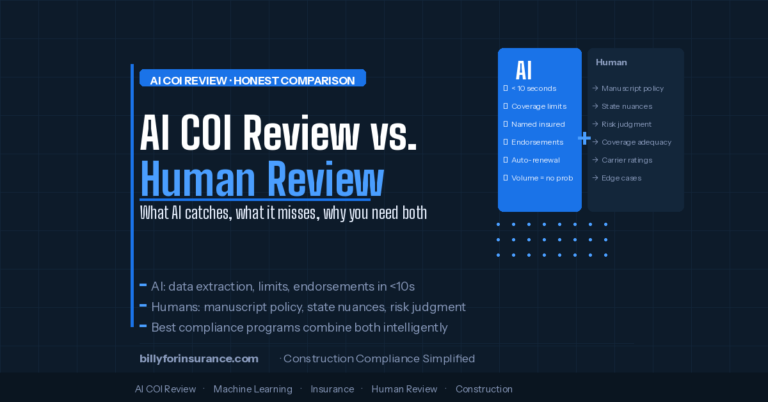

Blanket Additional Insured endorsements are widely accepted — but only when the written contract clearly requires AI status and the policy’s blanket language is triggered by that contract. Billy’s AI Review Assistant confirms whether blanket language is sufficient for your specific contract setup, not just whether it’s present on the document.

How to Verify a Sub Actually Has CG 20 10

This is where most GCs fail. Checking a box on a COI checklist that says “AI endorsement: yes” is not verification. Here’s what actual verification looks like:

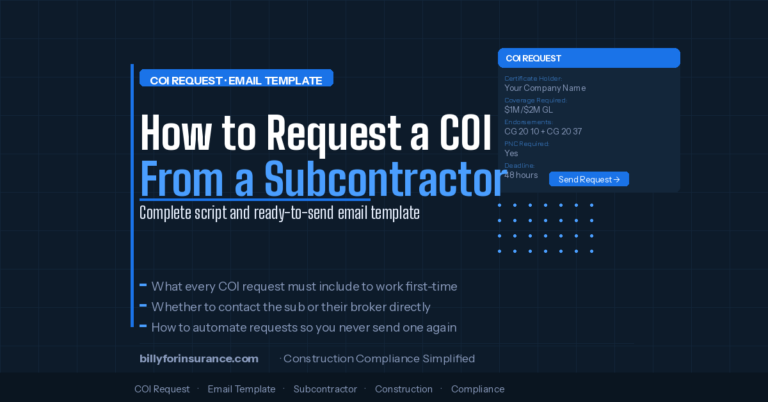

- Request the endorsement form, not just the COI — The ACORD 25 COI form will indicate that an Additional Insured endorsement exists, but to verify the form number, edition date, and specific language, you need the actual endorsement attached.

- Confirm the form number — Look for CG 20 10 specifically, or a non-ISO equivalent that provides equivalent coverage. “Additional Insured per written contract” language on the COI itself is not sufficient.

- Check the edition date — 04/13 is current. Note how it compares to your contract requirements.

- Confirm blanket vs. scheduled — If blanket, confirm your contract language triggers the endorsement. If scheduled, confirm your legal entity name is listed correctly (not DBA, not a related company).

- Verify completed operations separately — CG 20 10 covers ongoing operations only. If your contracts require completed operations coverage (and they should for most scopes), you need CG 20 37 as well.

5 Common Mistakes GCs Make With CG 20 10

1. Accepting a COI without the actual endorsement

The COI is a summary document. It is not the endorsement. Checking “AI endorsement” on the COI does not confirm that CG 20 10 is actually attached to the sub’s policy. Always require the endorsement form alongside the certificate of insurance.

2. Not requiring CG 20 37 alongside CG 20 10

CG 20 10 covers ongoing operations. Once your sub finishes work and leaves the site, their coverage under CG 20 10 terminates. Any claim that arises after completion — a roof leak six months later, a structural issue discovered during occupancy — requires CG 20 37 (completed operations). Most GCs require both; many forget to verify both are present.

3. Not specifying “primary and non-contributory”

Even with CG 20 10 in place, the sub’s policy may not pay first if you’re also named under your own GL coverage. Primary and Non-Contributory language makes the sub’s policy the first-payer, which is what your contracts almost certainly intend. Require it explicitly and verify it separately from the AI endorsement.

4. Not updating requirements when contracts change

If your standard contract language references a specific CG 20 10 edition, and ISO has released a newer edition since you drafted it, you may have a mismatch. Review your contract templates with your insurance broker or risk manager regularly.

5. Treating the initial COI as a permanent record

COIs expire. Endorsements expire with the policies they’re attached to. A sub who was fully compliant in January may not be compliant in October. COI tracking at scale means monitoring compliance continuously, not just at onboarding.

Stop Accepting COIs Without Verifying Endorsements

Billy’s AI Review Assistant verifies CG 20 10, CG 20 37, PNC, and Waiver of Subrogation on every submitted document — in seconds, automatically.

See How It Works →Frequently Asked Questions

Does CG 20 10 cost extra to add to a GL policy?

Typically very little — often $0 to $100 per year. It’s a standard endorsement that most carriers add at minimal or no cost. If a sub tells you they can’t provide CG 20 10, that’s worth investigating further.

What’s the difference between CG 20 10 and CG 20 26?

CG 20 26 is an older Additional Insured endorsement for ongoing operations. CG 20 10 replaced it in most contexts and provides similar (though not identical) coverage. If a sub submits CG 20 26, review it carefully with your broker before accepting it as equivalent.

Can a blanket AI endorsement replace a scheduled one?

In most cases yes, provided the written contract between you and the sub clearly requires AI status and the blanket endorsement language is triggered by that contract. The risk with blanket endorsements is that coverage depends on a contract being in place — if there’s any dispute about whether the written agreement exists or covers the right scope, coverage could be contested.

What happens if a sub doesn’t have CG 20 10 and a claim happens?

Without AI status, you have no right to tender the claim to the sub’s insurer. You’re left solely with your own policy, which almost certainly has a higher deductible and could result in increased premiums. This is precisely why endorsement verification — not just COI collection — is the foundation of real risk transfer in construction.