Every COI tracking platform now claims AI-powered review. Some use OCR with a marketing label. Others train actual models on insurance documents. The difference matters — and so does understanding what AI genuinely does well versus where human expertise is still essential.

The honest starting point: AI review is not a replacement for insurance expertise. But AI review that’s actually trained on insurance documents — not just OCR with a dashboard — is a genuine step change in what a lean compliance team can accomplish.

The question isn’t whether to use AI. At scale, manual review simply doesn’t hold up. The question is what kind of AI, paired with what kind of human oversight, produces real risk transfer rather than the appearance of compliance.

What AI Genuinely Does Well in COI Review

Data extraction at volume and speed

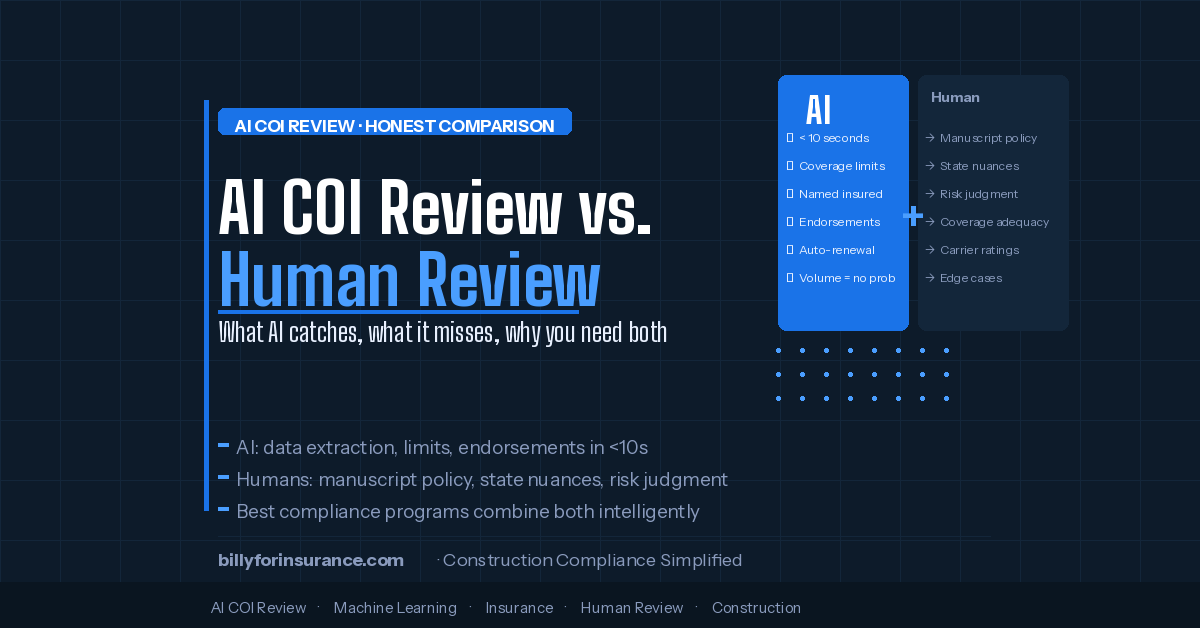

The most straightforward win for AI is extracting structured data from certificates at a scale and speed that human review can’t match. Named insured, policy numbers, coverage types, limits, effective dates, expiration dates, carrier names — AI pulls all of this from any COI format in seconds, without templates and without manual entry.

Coverage limit verification against requirements

Once AI has extracted coverage limits, it can instantly compare them against your project’s specific requirements. $1M/$2M GL required, sub submitted $1M/$1M — flagged. No human has to read that comparison. At 300 vendors, that’s 300 fewer manual comparisons per renewal cycle.

Endorsement presence detection

AI trained on insurance documents can identify whether CG 20 10, CG 20 37, and Primary and Non-Contributory language is present — not just whether the certificate notes them, but whether the endorsement form is attached. This is a critical distinction that OCR-based systems miss entirely.

Expiration monitoring and renewal outreach

AI doesn’t get distracted. It doesn’t miss a renewal because someone is on vacation. Automated monitoring of expiration dates and automated renewal outreach — 30 days in advance, to the sub and their broker — is one of the highest-value applications of automation in compliance. It prevents lapses instead of reacting to them.

Named insured verification

AI can flag when the named insured on a COI doesn’t match the legal entity name in the vendor record — one of the most common compliance errors in construction and one that’s nearly impossible to catch manually at scale.

Where AI Still Falls Short

Manuscript policy language and custom endorsements

Standard ISO forms are readable by AI trained on insurance documents. Manuscript policies — custom-drafted coverage that uses non-standard language — are a different challenge. When a sub’s policy uses non-ISO endorsement language that says roughly the same thing differently, AI may flag it as missing when a human expert would recognize it as equivalent. Edge cases require judgment, not pattern matching.

Coverage adequacy in context

AI can confirm whether limits meet minimum thresholds. It can’t assess whether those minimums are actually adequate for the specific risk profile of a particular scope on a particular project. A $1M GL policy may technically satisfy the contract requirement but be woefully insufficient for a high-rise curtainwall contractor. That’s a risk assessment, not a data verification — and it requires insurance expertise.

State-specific regulatory nuances

Workers’ Compensation requirements vary by state in ways that require regulatory knowledge, not just document reading. Texas workers’ comp is non-compulsory. Some states have specific additional insured restrictions. AI trained on general insurance documents may not reliably catch state-specific compliance nuances.

Carrier financial strength

Your contracts likely require insurance carriers to have a minimum AM Best rating. AI can read a carrier name from a COI. Confirming current AM Best rating against a live database is a separate step — one that requires integration with rating data, not just document review.

Speed without depth creates gaps. For teams managing hundreds of vendors, you need fast turnaround so vendors can be approved in hours, not days — and deep enough review to catch coverage gaps before they become claims. That combination requires both.

Billy Compliance TeamOCR vs. Actual AI: What’s the Difference?

| Capability | OCR-based systems | AI trained on insurance docs |

|---|---|---|

| Extract text from COI | ✓ Yes | ✓ Yes, more accurately |

| Understand policy language context | ✗ Text only, no interpretation | ✓ Interprets meaning, not just words |

| Identify endorsement forms by number | ⚠ Only if exact text matches | ✓ By form number and language patterns |

| Handle non-standard formats | ✗ Often fails without templates | ✓ Template-free extraction |

| Detect coverage gaps vs. requirements | ⚠ Basic limit comparison only | ✓ Full requirement stack review |

| Flag manuscript policy differences | ✗ Not possible | ⚠ Better, but edge cases still need human review |

Most COI platforms that claim “AI-powered” review are using OCR — optical character recognition — to extract text, then running rules against extracted fields. That’s automation, not AI. Genuine AI review means the system understands insurance document structure, policy language context, and endorsement semantics — not just whether a number in a field exceeds a threshold.

How Billy Combines AI and Human Review

Billy’s AI Review Assistant reads submitted COIs and endorsements against your contract requirements. It checks:

- Coverage types and limits vs. project requirements

- CG 20 10 and CG 20 37 presence, edition date, and blanket vs. scheduled status

- Primary and Non-Contributory language

- Waiver of Subrogation status

- Named insured accuracy against the vendor record

- Expiration date monitoring with automated renewal outreach

For self-service users, the AI handles the full review queue automatically — flagging deficiencies with specific remediation guidance sent to the sub or their broker. Most standard-format COIs resolve without any human intervention from the GC’s team.

For Managed Services users, licensed insurance professionals handle the edge cases that require judgment — manuscript policies, state-specific nuances, complex endorsement stacks, and situations where coverage adequacy assessment goes beyond document verification. The AI handles volume. Human experts handle complexity.

Self-Service AI vs. Managed Services: Which Is Right for You?

Self-service AI works best when…

Your compliance requirements are relatively standard, your team has some insurance knowledge to handle edge cases internally, and your primary need is volume — automating collection, tracking, and standard review at scale.

Managed Services works best when…

Your team has limited insurance expertise, you’re managing complex endorsement requirements or OCIP/CCIP programs, your volume is high enough that internal review capacity is a bottleneck, or you want licensed professionals accountable for compliance decisions.

See the full breakdown in our guide to self-service vs. managed COI tracking, including the 7 signals that it’s time to add managed services to your compliance program.

See AI Review in Action

Watch Billy’s AI Review Assistant process a COI — from submission to compliance status — in under 10 seconds.

Book a Demo →